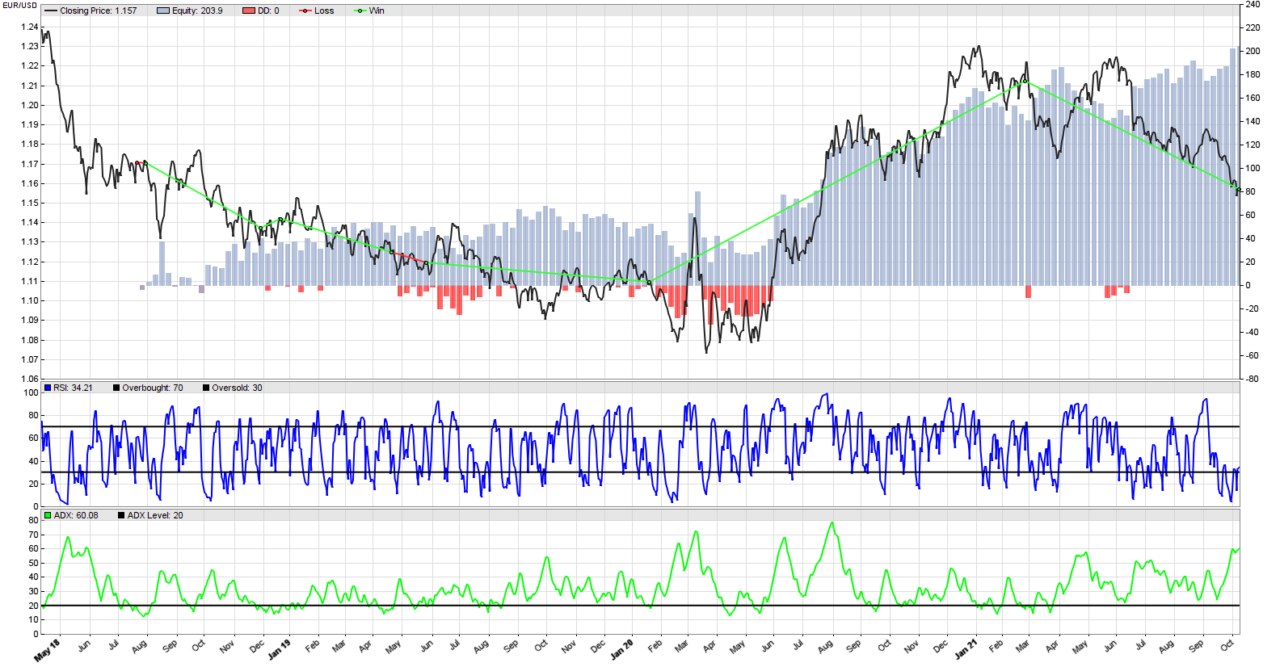

We managed to produce a terrific Zorro Trader back-test of our ADX and RSI trend following strategy on the mean-reverting EUR/USD pair. The equity curve is above, and the trades look beautiful. But the market does not rewards us for beautiful equity curves or impressive back-tests. It only rewards us for creating robust systematic trading strategies that work equally well in the future as they did in the past. And one important condition for that to happen is what we stated before: a strategy should not depend heavily on the values we set for its parameters.

by Algo Mike

Experienced algorithmic and quantitative trading professional.