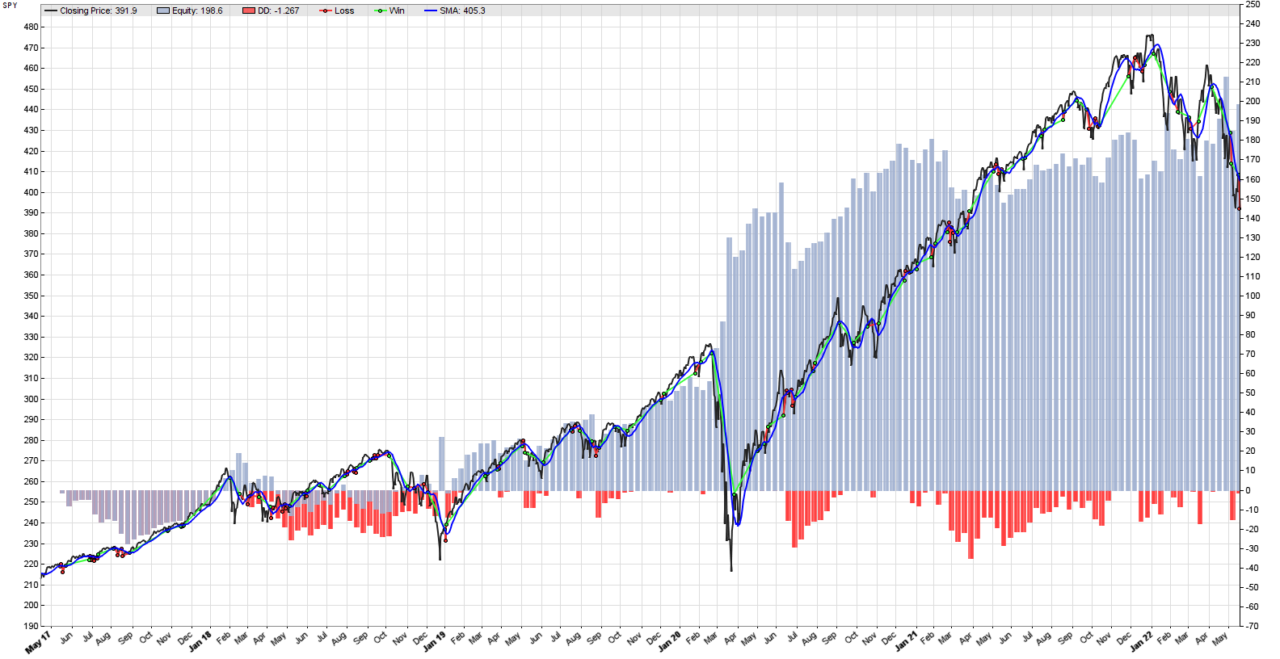

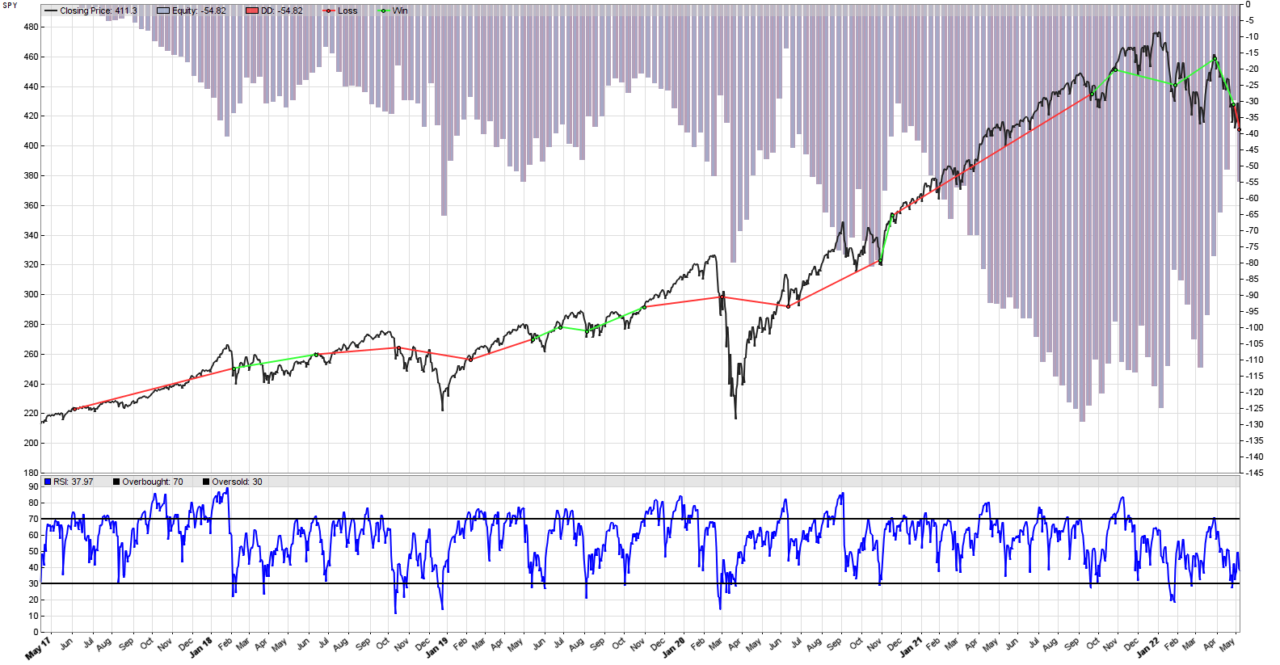

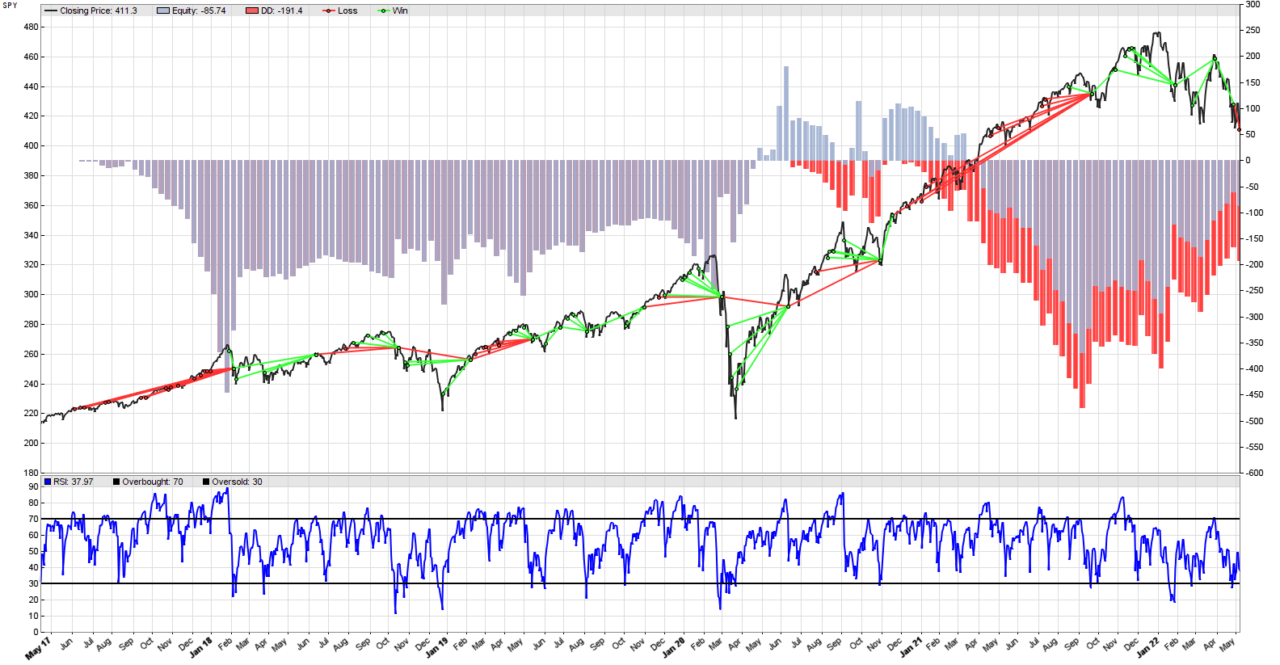

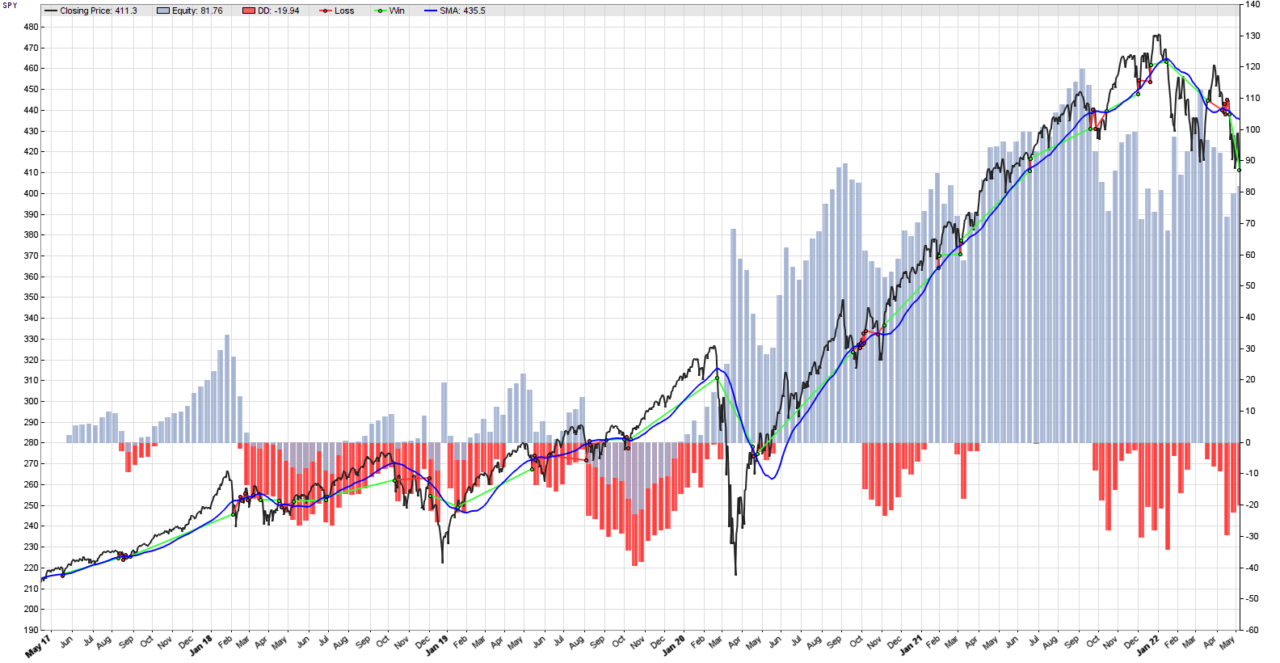

In this post, we will implement the simplest systematic trend following strategy in Zorro Trader, and we will run a back-test to measure its historical performance. The image above represents graphically the output of the strategy in a back-test. The underlying asset in this case is the SPY, an SP500 exchange traded fund (ETF). In plain English, the strategy can be expressed as follows: