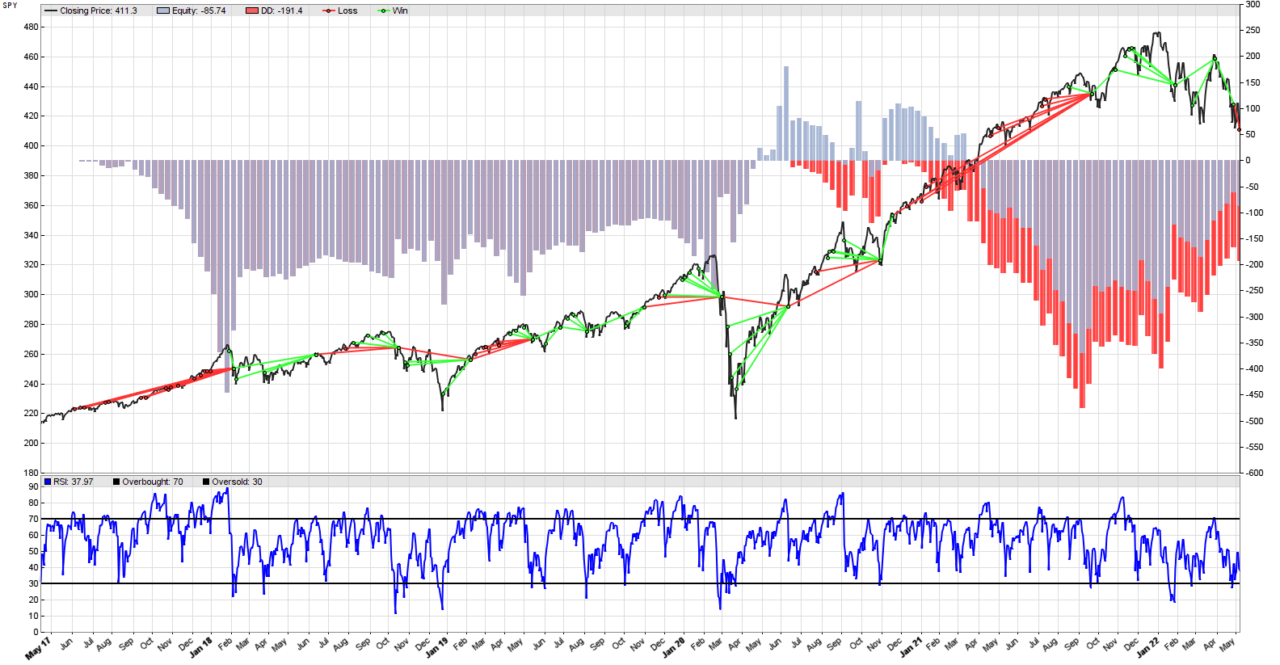

Mean reversion is the property of a time series to drift away from some mean (like a moving average), but then return to it. In a way, it is the opposite of a trend, which tends to continue for a while. In a sideways market, prices go up and down randomly, but their mean stays pretty much the same. Mean reverting behavior can be observed during some trends as well, but then the mean (moving average) is drifting up or down. Arguably, the simplest way to trade mean reverting markets in Zorro Trader is to use the RSI indicator. The result for SPY is in the picture above.

by Algo Mike

Experienced algorithmic and quantitative trading professional.