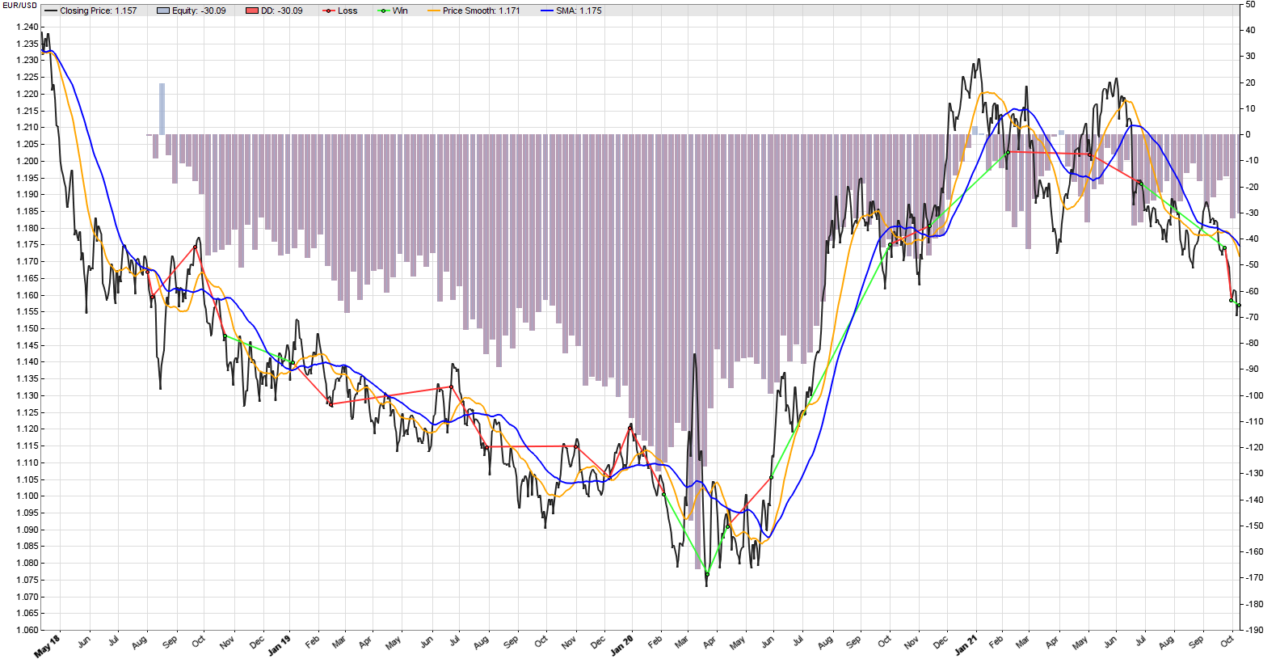

Trend following in mean reverting assets is notoriously difficult. We ran a back-test of our simple two moving averages trend following strategy (25 days and 50 days) on the EUR/USD FOREX pair in Zorro Trader. The result is in the image above. The equity curve looks terrible, and the strategy is on the wrong side of most of the trends. Time series that exhibit some degree of mean reversion do not lend themselves easily to moving averages trading strategies. But we know that there are some profitable trends in the price curve. We see them, but how can we trade them?

by Algo Mike

Experienced algorithmic and quantitative trading professional.