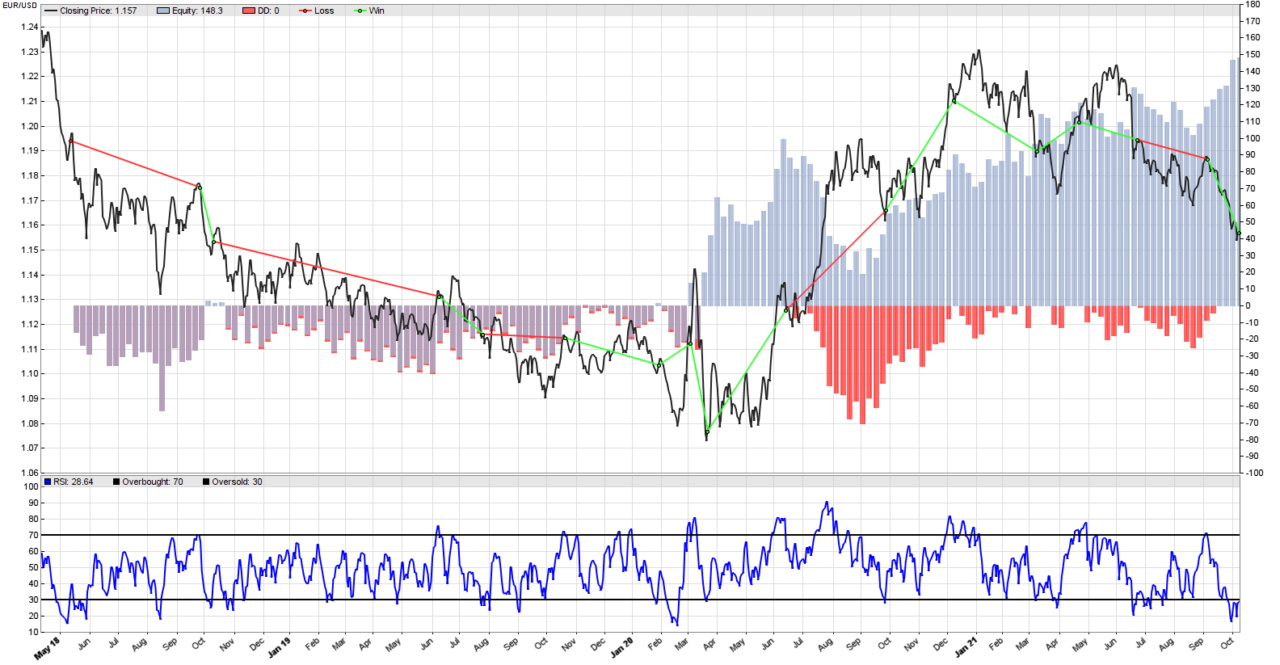

Remember the equity curve of our RSI mean reversion systematic trading strategy from the previous post (displayed above)? We were trading the EUR/USD Forex pair, and used a RSI formation period of 10 days. As you know, any technical indicator that needs a formation period will lag. The longer the formation period, the longer the lag. And we know that sometimes this lag can hurt our results. How about we analyze what changes when we change the RSI formation period in Zorro Trader? Maybe we can learn something useful from that.

by Algo Mike

Experienced algorithmic and quantitative trading professional.